Issue #50: Trade Idea – Short stETH

In this issue of Monetary Mechanics, I am going to do something a little different. In September 2021, I released a trade idea, which was to short CNH (the offshore version of the CNY). My thesis has played out more or less as I anticipated back then. While I did not foresee the recent waves of draconian lockdowns in China, I did manage to foresee a number of warning signs that were clear harbingers of the recent weakness in the Chinese currency.

In this issue of Monetary Mechanics, I am going to release another trade idea, but in the blockchain space this time. I have been thinking about this since the collapse of Terra (UST/Luna), and I believe that there is a favorable balance of risk and reward now.

My thesis is basically shorting wrapped stETH (wstETH) using wrapped ETH (wETH) as collateral on Euler. wstETH is a proxy for stETH, which is the staked version of ETH, and wETH is a proxy for ETH. Essentially, this is a market-neutral trade that could benefit during a more significant deviation in the stETH/ETH ratio.

What is Staked ETH (stETH)?

stETH is a claim on 1 staked ETH on the Ethereum Beacon Chain. The Ethereum Beacon Chain will serve as the consensus layer for Ethereum when the network switches from proof-of-work (PoW) to proof-of-stake (PoS) in an upcoming upgrade that is also known as “the merge.”

When one stakes ETH, one locks up ETH, which is an act that gives one the ability to participate in block proposals on the network. In addition, one also receives rewards for actions that help the network reach consensus, involving the running of software that properly batches transactions into new blocks, as well as the checking of the work of the other validators.

While there are several ways to stake ETH, only “liquid staking” is going to be explained below for sake of relevance. With liquid staking, one possesses an ERC-20 token that represents one’s share of the staked ETH, which allows one to trade into and out of a staked ETH position. For Lido, the largest provider of liquid staking solutions, this ERC-20 token is called stETH.

stETH automatically accrues all the staking rewards and penalties given to the validators on the Ethereum Beacon Chain.1 2

How Does One Get Staked ETH (stETH)?

There are several ways to get stETH.

First, one can deposit ETH into Lido’s smart contracts, which will give one newly minted stETH directly from the protocol.

Second, one can buy stETH on the open market from a variety of centralized exchanges (CEXs) (e.g. FTX, Binance, etc.), decentralized exchanges (DEXs) (e.g. SushiSwap, PancakeSwap, Uniswap, etc.), or decentralized exchange aggregators (DEX aggregators) (e.g. ParaSwap, 1Inch, Matcha, etc.).

What are the Main Advantages of Staked ETH (stETH)?

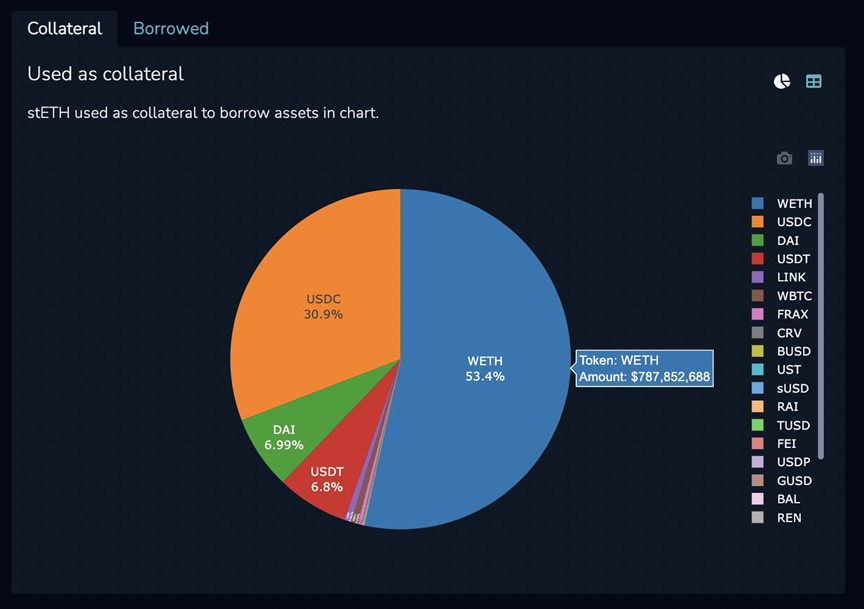

The main advantage of liquid staking over other staking solutions is that, with liquid staking, one is allowed to trade into and out of a stETH position whenever one wants. Moreover, stETH can also be used as collateral to borrow against because stETH is liquid and widely traded.

What are the Main Disadvantages of Staked ETH (stETH)?

In theory, stETH and ETH should trade at or close to a 1:1 ratio. In reality, a legitimate reason why the prices would de-peg is if the general consensus about the feasibility of the Ethereum network successfully transitioning from a PoW network to a PoS network changed (i.e. if the general public believes that the probability of “the merge” being successful is low). In that case, stETH would trade at a discount, because there would be a correspondingly higher risk that one would never get one’s original staked ETH back.

However, that does not seem to be what is happening here. The basic problem is that many users have used rehypothecated collateral to open a leveraged yield farming position, essentially leaving them long stETH and short ETH in the end.

Users would buy ETH from a CEX or DEX of their choice, deposit that ETH into Lido to mint new stETH, deposit that stETH into Aave as collateral, borrow ETH against stETH, deposit that new ETH into Lido to mint more stETH, deposit that stETH as collateral again, and so on and so forth. This leveraged staking position takes advantage of the yield generated from staking ETH, as well as the low costs of borrowing ETH. This is analogous to a levered carry trade.

The blow out of the stETH-ETH spread is most likely a result of the general chaos resulting from Terra’s collapse. While stETH is redeemable for 1 ETH and accrued staking rewards at the time of the Ethereum network’s successful transition, there is no way to unstake stETH. Consequently, this leveraged staking position is quite difficult to unwind – the only way to unwind this is to buy more ETH, which requires more funds in reserve.

What about the reverse? stETH is difficult to short, because stETH is a rebasing token, meaning that the supply of the token fluctuates on a daily basis. In addition, Aave has already disabled the borrowing of stETH, stopping users from taking the other side of the leveraged staking strategy.3

There is currently approximately $2.9 billion stETH deposited as collateral on Aave. The blow out of the stETH-ETH spread would trigger liquidations on anything borrowed against stETH. Trading below 0.9 stETH/ETH would begin to trigger those liquidations.

What is the Trade?

If you believe that this levered short volatility trade has a reasonable probability of blowing past some of these liquidation prices, then you should short stETH and long ETH.

How to Execute the Trade?

Euler allows you to borrow wstETH (wrapped staked ETH). The price of wstETH is indexed to the quantity of stETH according to the accrued staking rewards generated by the staking of ETH on the Ethereum Beacon Chain. Therefore, wstETH earns rewards via increasing price of stETH, rather than as a rebasing token and via increasing quantity of stETH.4 In other words, the price of wstETH/stETH should increase in line with the daily rebasing rewards of stETH.

In addition, the price of wstETH is also kept in line by an arbitrage opportunity available/accessible on Lido, should the price of wstETH ever significantly deviate from its indexed value.5

The current indexed value of wstETH/stETH is 1 wstETH/1.0713 stETH.

Euler only allows overcollateralized borrowing.

wETH has a collateral factor of 0.88.

wstETH has a collateral factor of 0.85.

DAI has a collateral factor of 0.85.

USDC has a collateral factor of 0.9.

Therefore, if you have $1,000 worth of wETH and you want to borrow wstETH, then the maximum that you can borrow is $1,000 × 0.88 × 0.85 = $748 worth of wstETH.

At this level of borrowing, the risk-adjusted value of your collateral is $1,000 × 0.88 = $880, and the risk-adjusted value of your liabilities is $748 ÷ 0.85 = $880.6

Assuming you want to execute this entire trade using DeFi applications, and you want to be 100% market-neutral relative to the price of ETH, your final positioning would be the following:

$1,000 wETH deposited as collateral on Euler earning 1.47% annualized.

$748 wstETH borrowed and sold short on Euler costing 4.93% annualized.

$337 DAI deposited as collateral on Euler earning 2.41% annualized.

$252 wETH borrowed and sold short on Euler costing 3.1% annualized.

Therefore, your net positioning would be long $748 wETH and short $748 wstETH using $1,337 of initial capital with (1 × 1.47%) – (0.748 × 4.93%) + (0.337 × 2.41%) – (0.252 × 3.1%) = approximately 2.19% annualized cost of carry.

Finally, note that these interest rates are subject to change over time and that these calculations are simply for an explanatory purpose and serve to provide an estimation of the cost to carry this position. I would expect the annualized cost of carry to range between 2% and 4%.

wstETH/stETH is currently trading at 1.0468, while the current indexed value of wstETH/stETH is 1 wstETH/1.0713 stETH, as mentioned above. From this, it is inferred that stETH/ETH is 1.0468 ÷ 1.0713 = 0.977, which is almost exactly equal to the stETH-ETH spread on curve.

If the wstETH-wETH spread increases, then the risk-adjusted value of your liabilities will increase to over $800, and your position will become eligible for liquidation, but your position may not necessarily be immediately liquidated.

On Euler, liquidations are performed by third-party liquidators who are economically incentivized by the opportunity to purchase a borrower’s collateral at a discount. Naturally, a higher discount means that a position is more underwater.

On Euler, Uniswap v3’s decentralized time-weighted average price (TWAP) oracles are used to determine the solvency of a user, as well as to calculate whether or not a loan is sufficiently overcollateralized. Uniswap’s TWAP is assessed using the geometric mean price of an asset over some interval of time (for both wETH and wstETH on Euler, this time interval is 30 minutes).

In general, TWAP is both a smoothed indicator and a lagging indicator of the trade price, which makes it more resistant against price manipulation attacks via the use of flash loans or flash bots that manipulate transactions “instantaneously” within the same block. In addition, TWAP is also more expensive to manipulate via the use of large market orders, because the manipulated price must be maintained for some period of time relative to the TWAP time interval.

What are the Risks of the Trade?

Smart contract risks – there is always the possibility of Euler being affected by hacks, exploits, and/or protocol bugs. While Euler has not been hacked or exploited thus far, there are unfortunately frequent hacks and exploits of DeFi lending and borrowing protocols, particularly the relatively new and complicated protocols. Euler is indeed relatively new compared with established competitors such as Compound, Maker, and Aave. However, Euler has already been audited by Sherlock, which has also provided up to $10 million for decentralized hack/exploit protection.7

Price oracle risks – different protocols use different price oracles, which might not use the same liquidity pool to pull prices from. The prices for wstETH on Uniswap v3, for wstETH on Uniswap v2, and for stETH on curve might all diverge from one another. Hence, the maintenance of the wstETH-stETH peg depends on arbitrage.

Network risks – large liquidation events tend to slow down blockchains and generate expensive gas fees as the network gets congested. Sometimes, transactions fail and/or are dropped. So, even in the event that the stETH-ETH spread blows out, liquidations might not occur in a timely manner.

Market risks – these markets are typically fairly small, illiquid, and inefficient, which might cause weird things to occur (an example is the stETH-ETH spread trading at above 1, even if it logically should not be doing that).

The information provided herein is for informational and educational purposes only. It should not be considered financial advice. You should consult with a financial professional or other qualified professional to determine what may be best for your individual needs. Monetary Mechanics does not make any guarantee or other promise that any results may be obtained from using the content herein. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence. To the maximum extent permitted by law, Monetary Mechanics disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations prove to be inaccurate, incomplete, unreliable or result in any investment or other losses. Content contained or made available herein is not intended to and does not constitute investment advice and your use of the information or materials contained is at your own risk.

For more information about Lido, see: https://blog.lido.fi/how-lido-works/

For more information about the mechanics of stETH, see: https://blog.lido.fi/steth-the-mechanics-of-steth/

Aave has done this specifically to enable this leveraged yield farming strategy. When a user deposits stETH into Aave as collateral, that user will continue to benefit from rebasing rewards, which means that the value of that user’s deposited collateral will continue to increase over time, assuming constant stETH prices. For more information, see: https://blog.lido.fi/aave-integrates-lidos-steth-as-collateral/

For more information about the mechanics of wstETH, see: https://help.lido.fi/en/articles/5231836-what-is-wrapped-steth-wsteth

To see the current indexed value of wstETH/stETH, see: https://stake.lido.fi/wrap?mode=unwrap

For more information about the calculations of risk-adjusted collateral and liability values, liquidation proceedings, and the technicalities of Euler’s operation, see: https://docs.euler.finance/getting-started/white-paper#asset-tiers

For the announcement, see: https://blog.euler.finance/euler-partners-with-sherlock-for-decentralized-exploit-protection-32e522baa265

For the audit report, see: https://github.com/euler-xyz/euler-audits/blob/master/smart_contract_audits/Euler_-_Sherlock_Report.pdf