Issue #43: Basel IV (!?)

In J.P. Morgan’s Q4 2021 earnings call, there was mention of something that surprised me greatly – the implementation of Basel IV.

In Issue #26 of Monetary Mechanics, I covered some (but not all) of the most important features of the most recent suite of financial legislations and regulations governing large dealer bank balance sheet construction and behavior in the post-GFC period. Here is a brief review below for the people who have not yet read that.

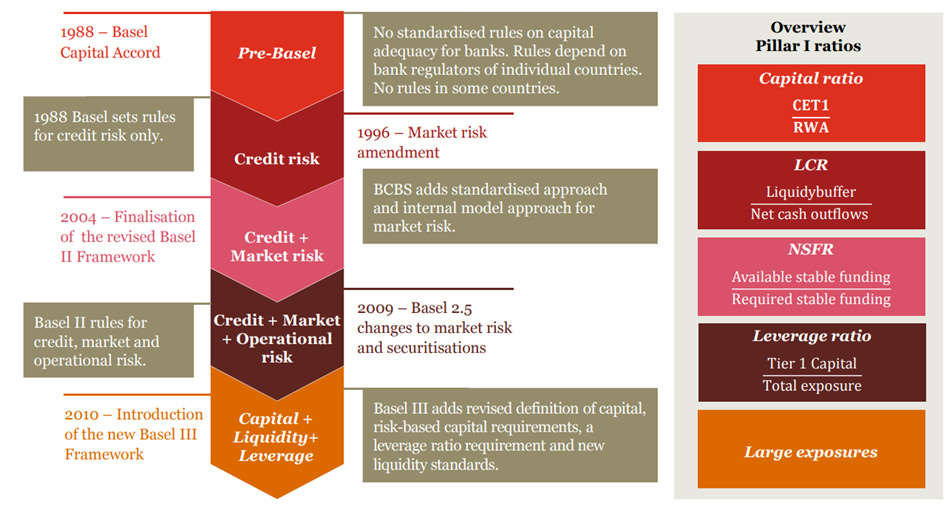

A History of the Basel Committee

The Basel rules are a set of international banking regulations, established by the Basel Committee on Banking Supervision (BCBS), headquartered at the Bank for International Settlements (BIS). The BCBS was created by the central bank governors of the Group of Ten (G10) countries as a response to the serious disturbances in international currency and banking markets caused by the fledgling Eurodollar system and the failure of Bankhaus Herstatt.1

At the outset, the objective of the Basel Committee’s work was to close the gaps in international supervisory coverage so that no banking establishment would escape banking supervision and that banking supervision would be consistent across member jurisdictions. As a result, the first capital measurement system, also known as Basel I, was approved by the central bank governors of the G10 countries and announced to banks in July 1988. Basel I called for a minimum ratio of capital to risk-weighted assets of 8% to be implemented by the end of 1992.

In June 1999, the Basel Committee released a proposal for a new capital adequacy framework to replace the old Basel Capital Accord of 1988. As a result, a revised capital adequacy framework, also known as Basel II, was implemented in June 2004.

The exploitation of the definition of “risk-weighted assets” was one of the primary driving forces behind the explosion of the use of securitized products just before the GFC.

Basel III

The need for a fundamental strengthening of the Basel II framework became extremely obvious, even before Lehman Brothers filed for bankruptcy in September 2008. As a result, Basel III was implemented in 2014. Basel III was much broader and more restrictive than its predecessors.

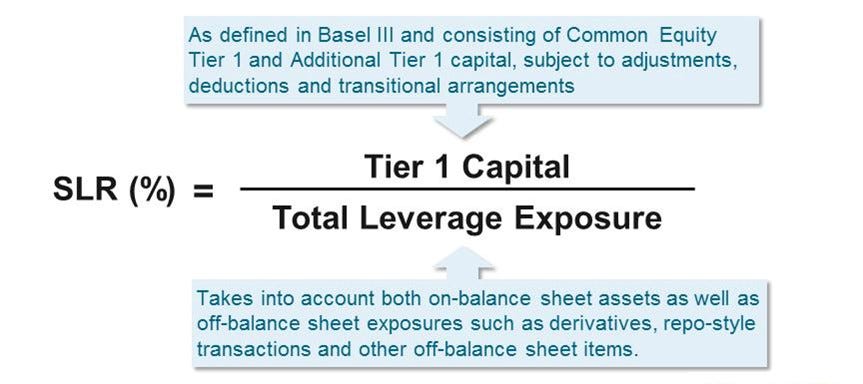

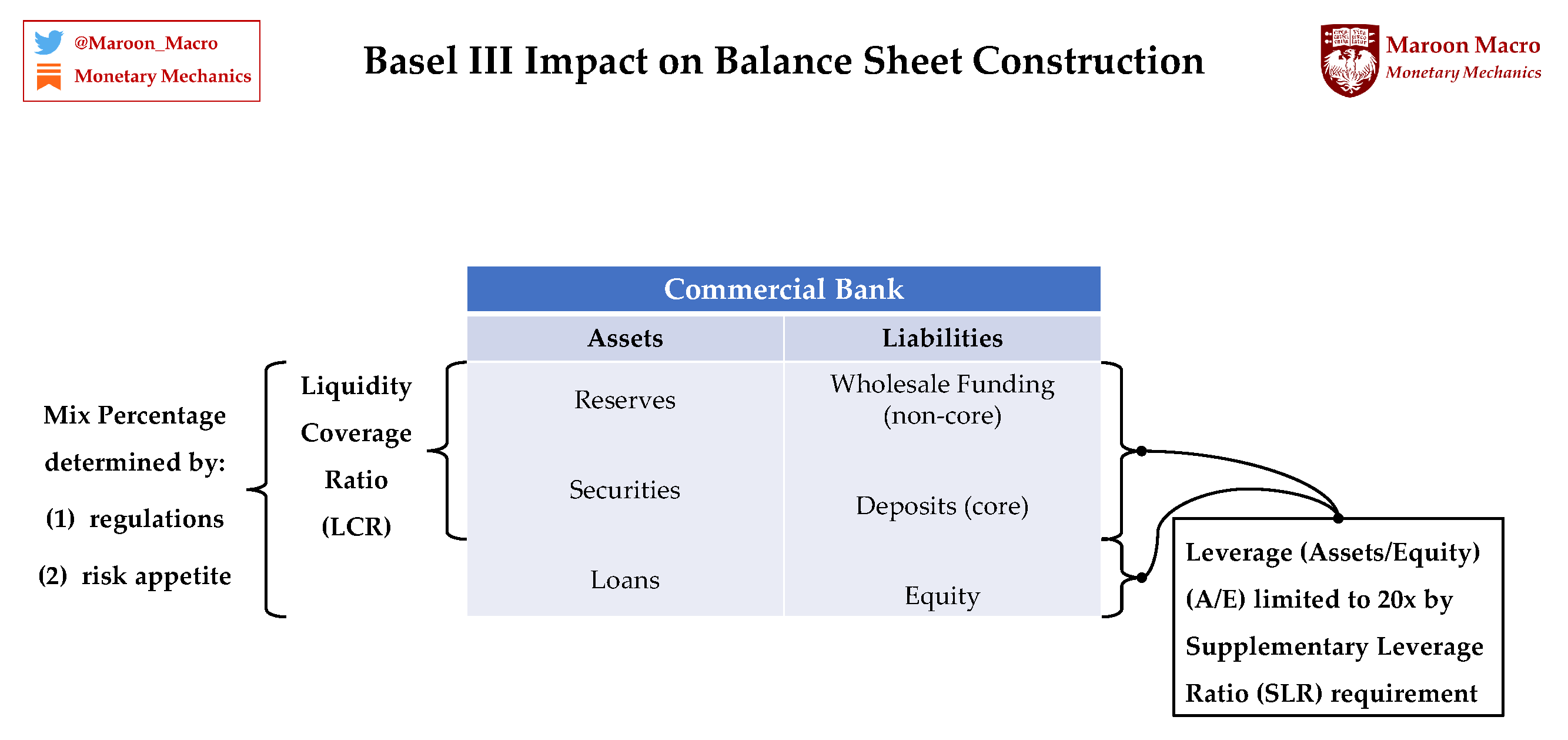

Basel III modified the original risk-weighted asset formula with the new supplementary leverage ratio (SLR) requirement. The SLR counts “total leverage exposure,” which includes both on-balance sheet and off-balance sheet exposure, and is also more importantly non-risk-weighted in its essence. While the exact calculation of “total leverage ratio” is laborious, long, and rather nuanced, the crux of the matter is that $1 of risky activity is treated as essentially similar to $1 of risk-free activity.

What this does is that this changes the profit incentives of large banks. Under the SLR, banks have become much more reluctant to provision their limited balance sheet space for activities that have traditionally been high-volume, low-margin, including repo intermediation. Consequently, because banks are now effectively limited to a maximum of 20x leverage on their Common Equity Tier 1 (CET1) capital, banks must now require a return on assets (ROA) of approximately 0.5% to meet a return on equity (ROE) target of 10%.

In a nutshell, the SLR forces banks to prioritize efficiency and profitability over growth. I am not going to argue about the appropriateness of such a policy, as that is a topic that is complicated and perhaps polarizing for people. Instead, I am only going to emphasize the effect that this policy has had, incentivizing banks to reduce their balance sheet intensity at the margins.

Back to Basel IV

So, if Basel III was all about restricting the increase of bank balance sheets via a flat leverage ratio, as opposed to a risk-weighted asset-based capital ratio, then what is Basel IV about?