Issue #37: An Obituary for LIBOR and the Transition to SOFR

With the start of the new year, the transition from the London Interbank Offered Rate (LIBOR) to the Secured Overnight Financing Rate (SOFR) is now officially underway, and I believe it would be timely to talk about some of the nuances involved in the process of transitioning away from LIBOR and towards SOFR as the new standard reference rate for a multitude of different financial contracts and securities.

According to a recent report published by the Alternative Reference Rates Committee (ARRC), which is a group of private market participants convened by the Federal Reserve Bank of New York (FRBNY) to facilitate a successful transition, there are approximately $223 trillion in total outstanding financial contracts, securities, and loans referencing USD LIBOR.1 Of that $223 trillion, $74 trillion will mature after June 2023, when LIBOR will be completely phased out (if everything goes as expected).

As of December 31, 2021, the one-week and two-month USD LIBOR rates have ceased to be published. However, the overnight and one-month, three-month, six-month, and 12-month USD LIBOR rates will continue to be published through June 30, 2023.2 In addition, as of December 31, 2021, all financial institutions are prohibited from entering into new financial contracts referencing USD LIBOR, with few exceptions (for example, certain types of hedging transactions are still allowed to reference USD LIBOR, subject to financial regulatory review).3

So, what is the big deal? Why are financial regulators trying so hard to replace one of the most important interest rates in modern capitalism? Why does it matter whether LIBOR or SOFR or some other alphabet soup interest rate is the primary reference rate for financial contracts?

There are two main reasons why financial regulators are attempting to transition away from LIBOR and towards SOFR as the primary reference rate for financial contracts:

Since the GFC, the unsecured interbank funding/financing market, the market from which LIBOR derives its interest rate, has basically completely dried up.

Scandals surrounding the calculation of LIBOR have tainted the way the general public perceives LIBOR, engendering mistrust of the entire IBOR rate complex.

The figure below shows how little volume is still traded in the interbank lending market today compared to when LIBOR was in its heyday. One would have to go back to the 1970s to find trading volume small enough to be even comparable to that of the post-2015 period. The percentage of all commercial banks’ total assets funded/financed via interbank borrowing fell all the way to 0.3% in 2018, compared to almost 5-6% in the 1990s and the early 2000s.4 Thus, it is indisputable that the interbank lending market today is hardly as deep and liquid as it used to be before the GFC.

The tweet thread below shows the widespread sentiment of mistrust of LIBOR, albeit in a somewhat joking manner, especially after post-GFC scandals exposed that the setting of the LIBOR rate was influenced/impacted by possible biases and personal financial incentives.5

In addition, another subtle and often underappreciated motive behind the move away from LIBOR and towards SOFR is banks’ own unwillingness to submit bids in the wake of the crackdown on perceived LIBOR manipulation.6 While the official reason for the reduction in the number of bids is not revealed, it is not difficult to realize that the costs of potential lawsuits very heavily outweigh the practically nonexistent benefits from submitting bids.

What is the London Interbank Offered Rate (LIBOR)?

What exactly is LIBOR – and why all the fuss around it?

Let’s begin with the basics:

The London Interbank Offered Rate (LIBOR) is a measure of short-term, unsecured, wholesale interbank borrowing costs. I am going to break down piece by piece exactly what this means, as I find that most mainstream financial media outlets tend to be a bit vague on the important details.

There are several different rates published within the greater IBOR rate complex that pertain to multiple jurisdictions. The most important rate is USD LIBOR, which is the cost of borrowing US Dollars (i.e. Eurodollars) from London banks. There are also GBP, EUR, CHF, and JPY LIBOR, which are the costs of borrowing those currencies from London banks.

While London IBOR rates are the most widely used, other IBOR rates are also published in other financial centers outside of London. Examples include SHIBOR, HIBOR, and TIBOR, which are the costs of interbank borrowing in Shanghai, Hong Kong, and Tokyo respectively.

What exactly is “short-term, unsecured, wholesale” interbank borrowing?

Short-term: LIBOR tenors range from overnight to 12 months at the longest, which makes it a measure of relatively short-term interbank borrowing costs that covers the entire money market maturity spectrum. The most used tenors are typically the overnight and the 3-month ones.

Unsecured: LIBOR rates measure the costs of unsecured (i.e. uncollateralized) interbank borrowing, which makes it an important barometer of credit risk. Because loans are unsecured/uncollateralized, the costs of interbank borrowing are significantly influenced by banks’ reputations, so LIBOR rates increase significantly during times of financial market stress. This is also one of the most important reasons why LIBOR is used as the reference rate for hundreds of trillions of dollars of financial contracts, securities, and loans. Because LIBOR acts as a base level of implied private sector default risk, all other rates can then be tiered in terms of riskiness relative to LIBOR (i.e. LIBOR + 100 bps), not unlike corporate credit spreads.

Wholesale: LIBOR rates measure what it costs for large banks to borrow from other large banks, which makes it a wholesale measure. I have already covered the definition and significance of “wholesale finance” in various previous issues (Issue #11, Issue #16, Issue #28, and Issue #33) of Monetary Mechanics. Importantly, prior to the GFC, the wholesale nature of LIBOR meant that people automatically assumed that most LIBOR counterparties were some of the most sophisticated, solvent, and liquid institutions in the world, which made them the best positioned to capitalize on low borrowing costs, as well as the most likely to repay those borrowing costs.

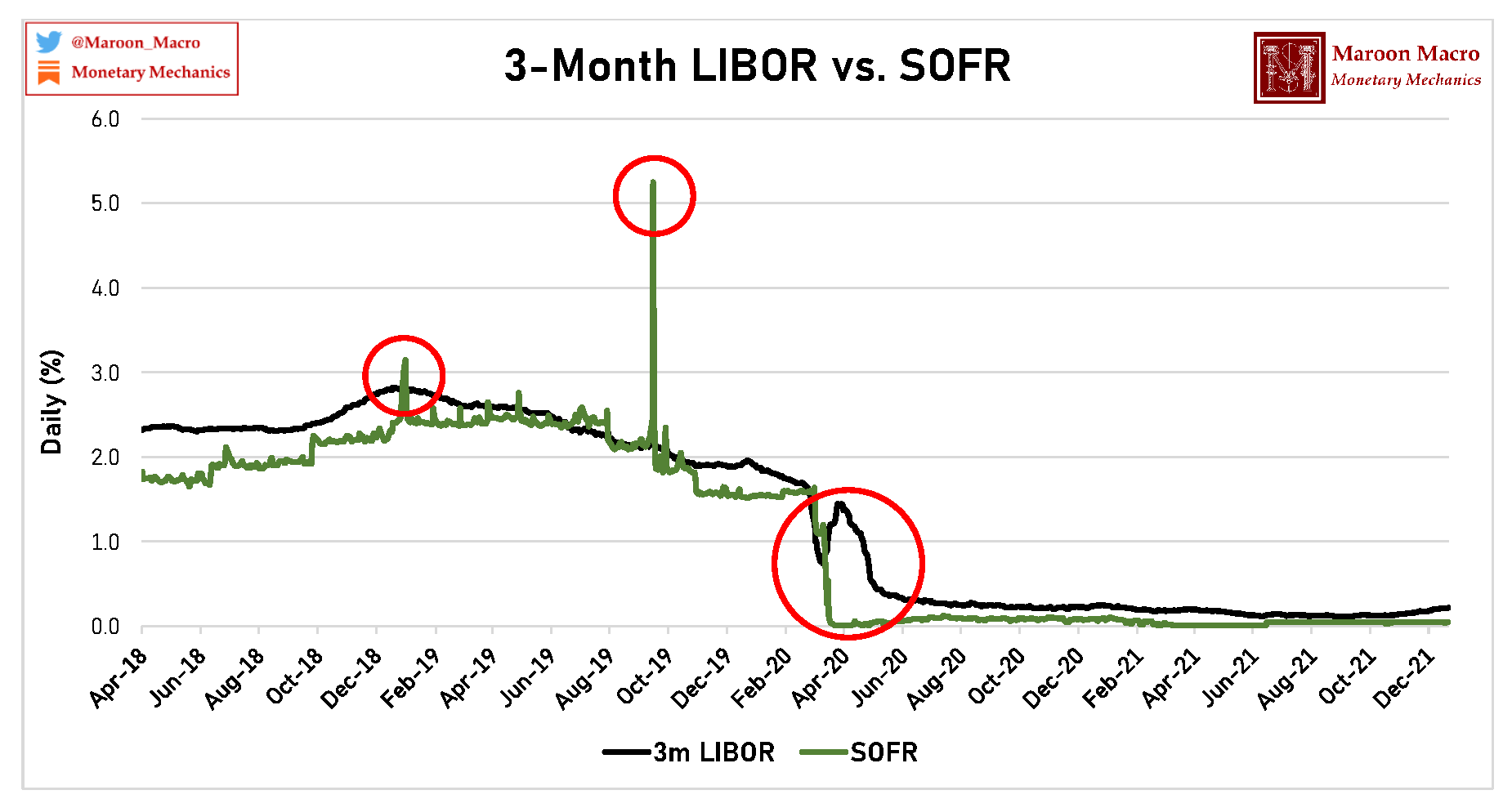

While there are not a lot of transactions that actually underpin the rate that LIBOR is supposed to represent anymore (see the first figure), it is still a relatively good proxy for credit risk in the private sector (i.e. it still behaves the way one would expect a credit-sensitive benchmark to behave – rising during periods of financial crisis and falling during periods of financial calm).

This stands in stark contrast to SOFR, which frequently behaves erratically due to certain idiosyncrasies in its construction, which I will cover later in this issue of Monetary Mechanics.