Issue #17: Banks, Dealers, and Bank Holding Companies – The Who’s Who of Financial Entities

Throughout the course of my formal education (and self-education) in financial history and the gradual growth of my understanding and appreciation of the complexity of the modern monetary and banking system, I have frequently experienced both confusion and frustration over the vast array of terms and definitions used between financial market participants and in the financial press. Oftentimes, these terms and definitions are used inconsistently and interchangeably in seemingly contradictory ways (perhaps with intentional ambiguity), so it is not always obvious what one means precisely when one says “dealer bank” or “broker-dealer.”

While a comprehensive study of the historical development and significance of the transition of commercial banks towards non-banking behavior and the transition of non-banks (primarily broker-dealers) towards banking behavior warrants its own separate issue, I will try to cover some of the most salient and relevant concepts in this current issue of Monetary Mechanics.

Savings and Loan Institutions (a.k.a. S&Ls, savings banks, savings institutions, or thrift banks/institutions) – provide many of the same services to customers as regular commercial banks, including deposits, loans, mortgages, and debit cards. However, unlike regular commercial banks, S&Ls specialize in savings accounts, residential mortgages, and working with individuals (as opposed to working with large businesses and unsecured credit services such as credit cards). S&Ls are either public or private and owned by their depositors. S&Ls used to play a far more prominent part in the financial system before the 1990s, but because of the disintermediation of traditional banking services and the transition towards “market-based finance,” S&Ls play an extremely diminished and minor part in the US economy today.

Credit Unions – provide many of the same services to customers as regular commercial banks, including deposits, loans, and other financial services. However, credit unions are unique in the sense that they are private and collectively owned by the members of a cooperative and operated on a not-for-profit basis. Customers must meet specific criteria to be eligible, often based on their affiliation with a certain community, business, or union. Customers are considered members of the credit union, so “making deposits” is regarded as “buying shares” in the credit union. Customers are paid dividends on the credit union’s earnings, like shareholders are paid dividends on the company’s earnings.

Commercial Banks – provide a wide range of financial offerings, including deposits, loans, mortgages, debit cards, credit cards, wealth management, and (recently) investment banking services. Commercial banks tend to focus on making and managing loans targeting the maintenance and expansion needs of regional, national, and international businesses. Commercial banks specialized in short-term business credit but have since become the “department stores” of the financial services world today. Commercial banks are typically large, public, for-profit corporations. Commercial banks are generally what comes to one’s mind when one thinks of a traditional “bank.”

Investment Banks – underwrite new debt and equity securities for all types of corporations, governments, and other entities, as well as facilitate mergers and acquisitions (M&As), restructuring, and the sale of securities. Investment banks connect investors in capital markets with financial institutions seeking capital market funding/financing. During the GFC, some of the more important independent investment banks (e.g. Goldman Sachs and Morgan Stanley) successfully converted to BHCs in order to gain access to the Federal Reserve’s emergency lending facilities (since the Federal Reserve supervises BHCs but does not supervise independent investment banks and broker-dealers). Other investment banks merged into larger preexisting BHCs (e.g. Bear Stearns, who merged into JPMorgan Chase, and Merrill Lynch, who merged into Bank of America). Other investment banks went bankrupt and failed (e.g. Lehman Brothers).1 2 Investment banks that are not a subsidiary of a BHC are not supervised by the Federal Reserve and do not have access to reserve accounts with the Federal Reserve.

Depository Institutions – a financial institution that is legally allowed to solicit and accept monetary deposits from the general public. In the US, depository institutions include S&Ls, credit unions, commercial banks, and limited purpose banking institutions such as credit card banks, industrial loan banks, and trust companies.

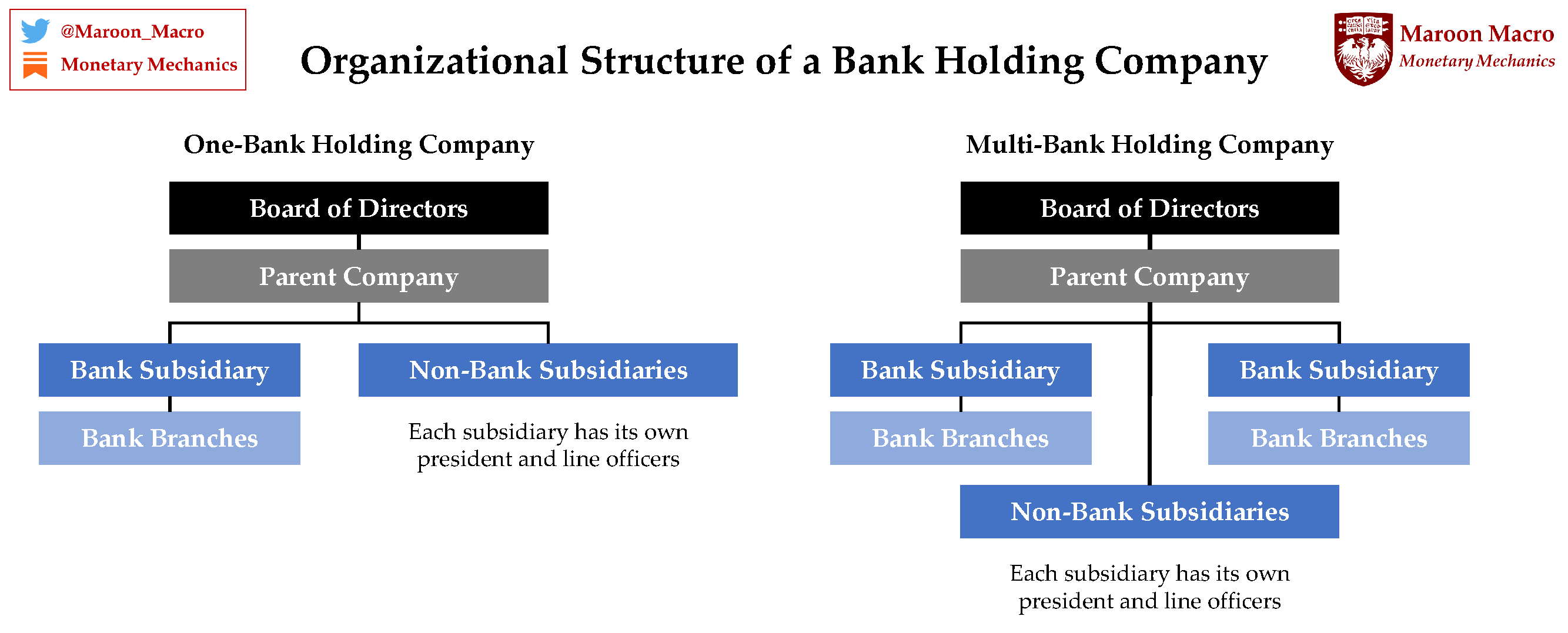

Bank Holding Company (BHC) – a corporation that owns a controlling interest in one or more banks but does not offer banking services itself. BHCs do not perform the day-to-day functions of the banks that they own. However, BHCs exercise control over the company management policies of the banks that they own. BHCs are regulated by the Federal Reserve. Banks that are not owned by BHCs are regulated primarily by the Office of the Comptroller of the Currency, though US banking regulations are so (purposefully?) convoluted that a total of five federal agencies are involved.

The Bank Holding Company Act of 1956 established bank holding companies as a financial entity. In the late 1960s, one-bank holding companies are established, which granted banks greater freedom and the ability to branch out from their dependence on individual depositors to other types of banking activities such as commercial paper and (eventually even) repo. This act was partially responsible for the expansion of permissible banking and bank-like activities, allowing for a more flexible and efficient management of a bank’s balance sheet structure, which resulted in the explosion in “liability management” in the 1950s-70s.

Financial Holding Company (FHC) – a bank holding company that can offer non-banking financial services such as securities underwriting, insurance underwriting, merchant banking, and investment advisory services.

The Gramm-Leach-Bliley Act of 1999 enabled bank holding companies to register as financial holding companies, which then enabled bank holding companies to engage in an even wider range of financial activities such as securities underwriting, insurance underwriting, and merchant banking activities. The Gramm-Leach-Bliley Act of 1999 repealed large segments of the Glass-Steagall Banking Act of 1933 and the Bank Holding Company Act of 1956, amending the rules, allowing commercial banks, investment banks, insurance companies, and brokerages to merge, and consequently creating a new structural framework for banks.

Brokers – execute trades on behalf of others, acting as an “agent” that is acting on behalf of investors. Brokers exist as a legal entity through which investors, holding brokerage accounts, engage in securities trading. Brokers bring buyers and sellers together for trade. Brokers are typically paid on trade commissions. Brokers never position instruments and securities themselves and only provide a communication channel/network that links financial market participants who are frequently numerous and geographically diverse and dispersed.

Dealers – execute trades on behalf of themselves, acting as a “principal” instead of an “agent.” Dealers typically make their profit through market making instead of on trade commissions. Dealers make markets in various instruments and securities by quoting bids (to issuers, to investors, and to each other) and asking prices at which they are prepared to buy and sell.

Broker-Dealers – frequently, companies perform both brokering and dealing functions under the same roof. While there are several large primary broker-dealers that are obligated to participate in US government debt auctions (about 20), there are also many small independent broker-dealers operating in the US (about 3,500). In addition, many broker-dealers offer investment banking services such as securities underwriting and dealing.

I am aware that there is a lot of misunderstanding surrounding the distinction between commercial banks and investment banks/securities broker-dealers. Both investment banks and broker-dealers do not themselves have direct access to reserve accounts with the Federal Reserve. If they are housed under the same corporate structure as a depository institution in a larger BHC/FHC, it is through the depository subsidiary (usually a commercial bank) that they are granted indirect access to the discount window, as well as reserve balances at the Federal Reserve.

Consequently, the Federal Reserve must implement monetary policy simultaneously through two channels in order to effectively influence the whole economy: the financial economy channel (via the primary dealers) and the real economy channel (via the commercial banks).

https://www.federalreserve.gov/newsevents/pressreleases/bcreg20080921a.htm

https://www.marketwatch.com/story/goldman-sachs-morgan-stanley-to-become-bank-holding-companies

Very good post. Perfect

how do i subscribe to premium?