Issue #2: Collateral’s Role in the Modern Financial System

Collateral flows lie at the heart of any proper understanding of market liquidity, and hence of financial stability. No other market is so critical to the functioning of the financial system, and yet so poorly understood. In addition, though, as policymakers begin to acknowledge the inadequacies of traditional theories of money and lending, collateral flows are increasingly recognized to be just as important a driver of credit creation as money itself. Despite this, a true appreciation of the importance of collateral flows is hampered by the inadequacy of the way in which they are accounted for.1

Money has historically been defined as a subset of bank liabilities (physical currency, deposits, etc.). Our modern financial system is not that different, although sometimes it appears radically so.

Banks, since engaging in “liability management,” have ceased to be limited by static deposit pools. Now, the size of banks’ balance sheets is constrained by more abstract measures – VaR, risk weightings, repo funding, etc.

In this wholesale banking model, the ability to access funding markets is paramount. When significant portions of one’s balance sheet are funded on a rolling short-term basis, “possession” of pledgeable collateral to access repo financing is how one lives to fight another day. Other types of short-term funding are equally as important (including commercial paper and FX swaps), but for now, in this issue of Monetary Mechanics, I will focus on collateral.

Collateral can be either public (US treasuries, agency securities, other sovereign bonds, etc.) or private (mortgage-backed securities, asset-backed securities, corporate bonds, structured products, etc.). High-quality collateral can be defined as a financial asset that can be used to rapidly secure cash borrowings at minimal haircut (i.e. cash equivalent). There are many other types of collateral, but many of these can and will be repudiated by the repo market during times of significant market stress or be subjected to unacceptably high haircuts. Thus, this makes high-quality collateral the most important type of collateral.

Aside from being used to secure short-term funding, collateral is also used to underpin a variety of derivatives transactions and used to leverage (primarily fixed income) portfolios. Now, after the passing of Basel III and Dodd-Frank legislations/regulations, high-quality collateral is also used by banks to ensure that they stay legally solvent and compliant with these stricter regulatory requirements.

An important part of collateral management is something called “rehypothecation,” “repledging,” or “reuse.”2 Rehypothecation allows a single security to be reused by multiple parties. In doing so, rehypothecation targets the problem of the total quantity of collateral being insufficient to cover the demand for leveraged structures and regulations that require collateral at any given time. While it may seem strange and unbelievable on the surface, it is indeed substantiated by various examples from the Federal Reserve and IMF.3 4

Rehypothecation is in essence analogous to the traditional money-creation process (i.e. fractional reserve banking, lending leads to deposits which leads to more lending, based on reserve requirements, etc.). In this world, high-quality collateral serves as “high-powered” base money. However, a critical difference in this non-traditional money-creation process is that it depends entirely on banks to trust each other. New credit can be created only with the occurrence of onward pledging, which depends on, for example, Goldman Sachs’ trust in Credit Suisse. If there is heightened counterparty risk, onward pledging may not occur, resulting in a shadow deleveraging.5

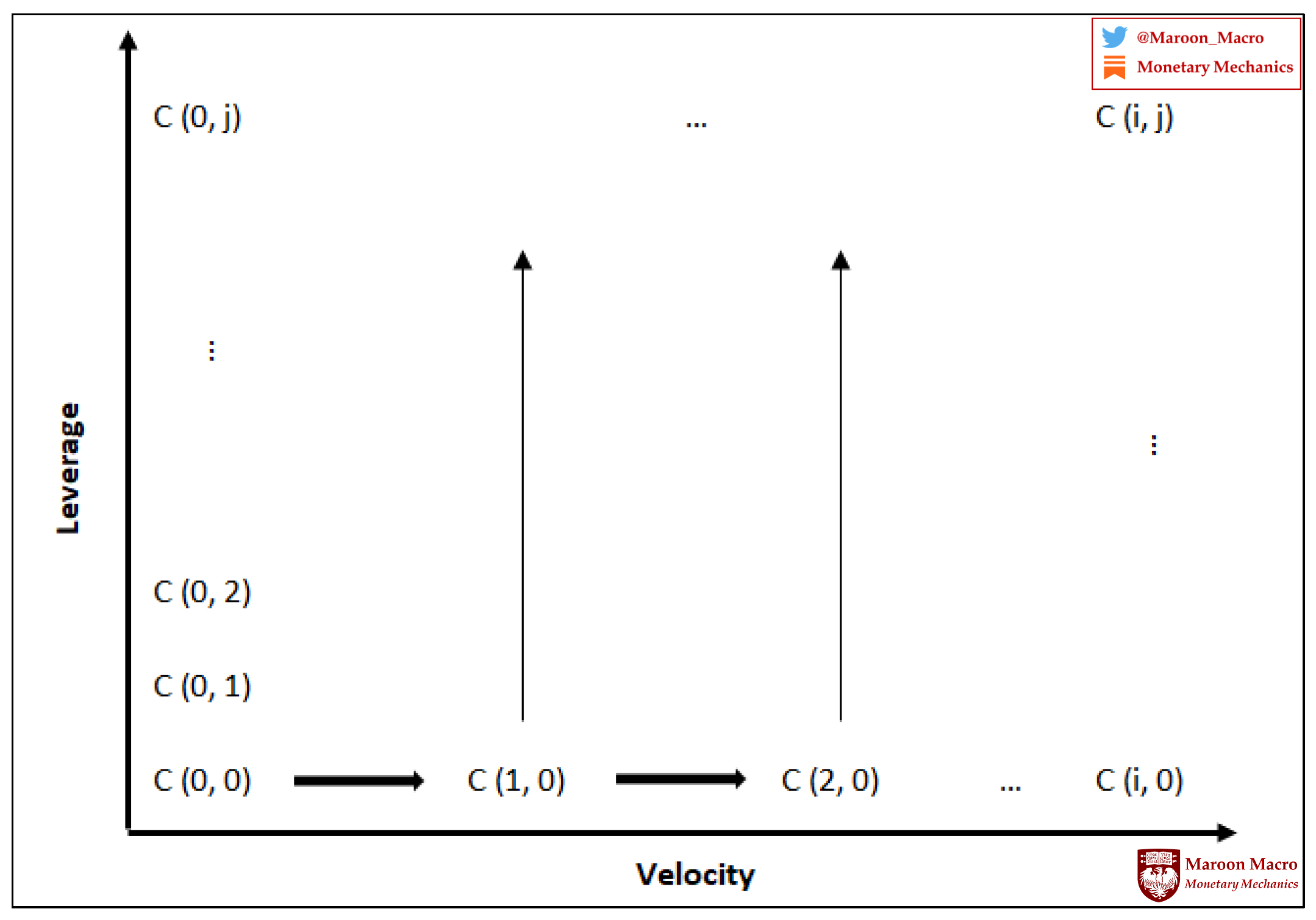

Because of the permissive ability of counterparties to reuse collateral, one could say that there is a horizontal leverage multiplier (velocity determined) and a vertical leverage multiplier (haircut determined).

Haircuts determine how much leverage can be obtained using a specific class of collateral as it denotes the overcollateralization that must be provided by the cash borrower. As a simple example, if agency MBS have a haircut of 5%, then an investor must put up $5 of their own capital for every $100 of MBS they want to buy and fund in repo. Thus, a 5% haircut implies 20x potential leverage. In practice, this limit is typically never reached. Mortgage real estate investment trusts (mREITs), who invest in agency MBS, run leverage ratios around 7-10x. Relative value funds, which are hedge funds who invest in treasury securities of various maturities, run leverage ratios around 20x (since the haircut on treasury securities is usually 2% or less).

These securities, because they are funded via the repo market, can then be reused by the dealer (who receives them from the investment fund) for the dealer’s own funding needs, to close out existing positions, or to lend them out to another customer/client for shorting purposes. Thus, each user of the security can support their own vertical leverage multiplier, while the number of users determines the size of the horizontal leverage multiplier.

I think of repledging and rehypothecation like Shroedinger’s collateral – a single collateral security spread over multiple transactions, but when one actually goes looking for it, it collapses into a single security.

However, it is important to note that not all collateral can be reused, and not all collateral that can be reused is always reused. There are limits to reuse and rehypothecation in the United States, but not in the UK or Europe.6 In theory, a piece of collateral could be reused an infinite number of times by broker-dealers registered in the UK or Europe. In practice, however, limits are individually negotiated between private parties through bilateral contracts and bespoke agreements.

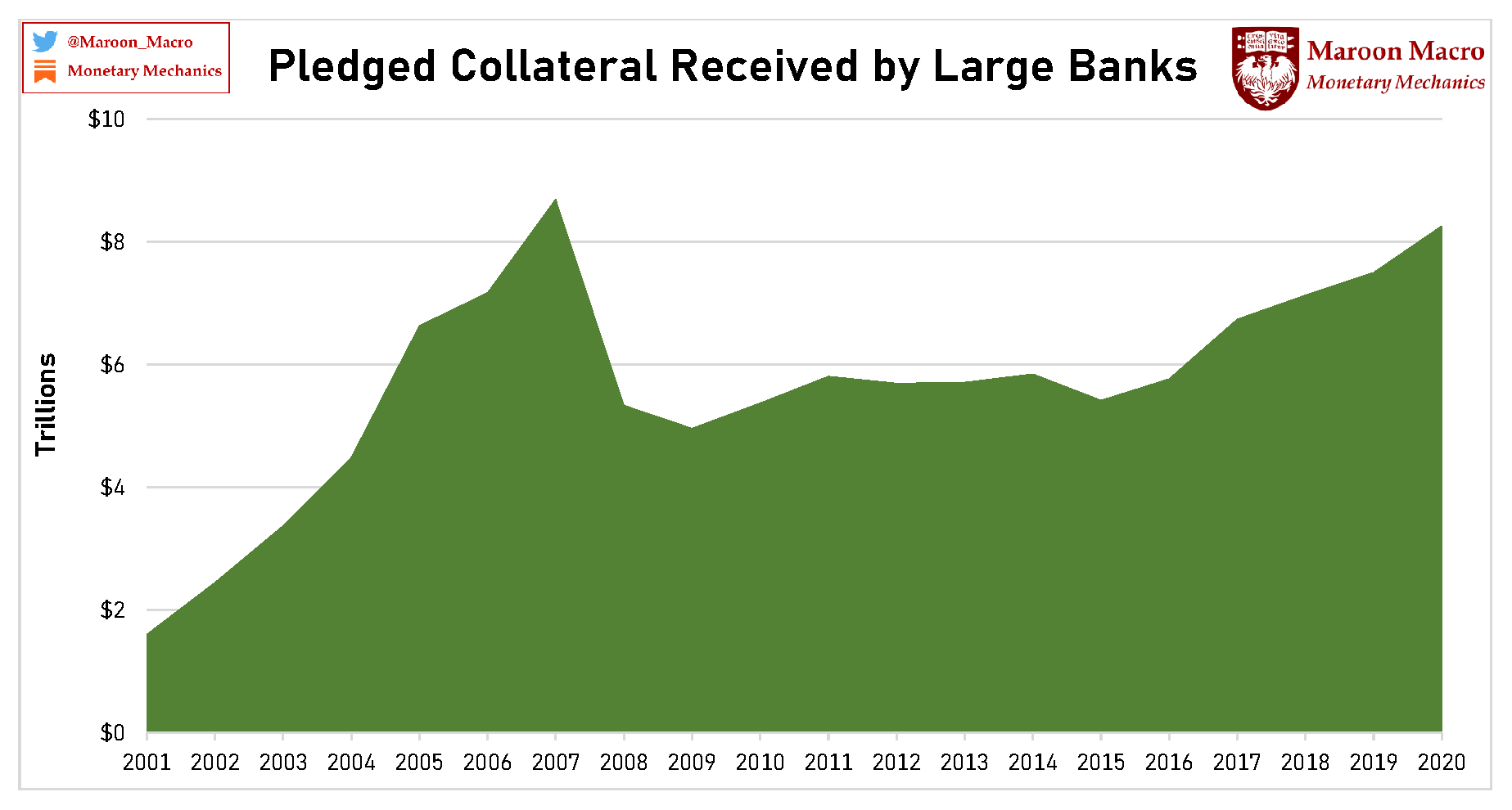

Collateral use and reuse in financial markets is extensive. Before the Lehman collapse, the volume of funding via pledged collateral was about $10T, which was even higher than the M2 at that time.7 Moreover, the accounting of pledged collateral suggests that many banks were (and still remain) funded via collateral (via their transition to “liability management” as mentioned above). Lehman’s last annual balance sheet size was $691B, but the pledged collateral that Lehman received and could have reused was $798B. These numbers were not unique or unusual among other banks during this time.

We already have very good data about tri-party repo in the United States. However, the more important, international, Eurodollar market is the bilateral repo market, the market in which “unlimited” rehypothecation can occur. Unfortunately, this is also where we have very little and limited data collection and analysis to work with.8 9 10

Similar issues exist for other short-term funding markets, such as when the BIS discovered that a multitude of foreign financial institutions owed more than $10.7T of non-bank off-balance sheet dollar obligations, a number that likely exceeds these same institutions’ on-balance sheet dollar debt.11

Traditional economic theory does not consider credit to be money (i.e. included in the M2 money supply), because it assumes that any credit that could lead to spending would eventually wind up as forms of bank deposits (and thus be part of M2). However, through the repledging and rehypothecation of collateral, and the resultant creation of “collateral chains,” additional purchasing power is created in the financial economy without a need for the creation of any additional bank deposits, bank reserves, government debt, private debt, or anything else for the matter. Basically, all it takes is for User A to accept collateral from User B, then for User A to then repledge this security to User C for a separate transaction.

Furthermore, unlike traditional money creation, collateral credit creation does not rely on the central bank’s lender of last resort assurance. There is no possible way for the Federal Reserve or other central banks to intervene in this process. In the event that haircuts rise, collateral chains shorten, or the supply of collateral shrinks, deleveraging will occur in the financial system. The increasing of the quantity of bank reserves does not matter and will not change anything, as bank reserves cannot be used as collateral.

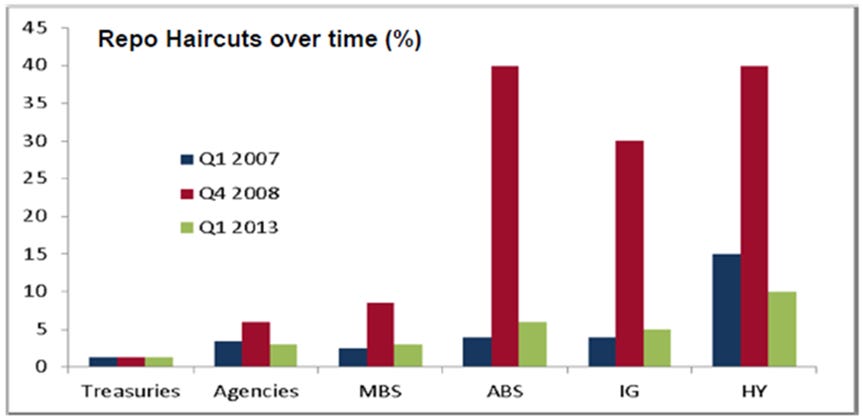

There are several features that define the boundaries of risk in this market: haircuts, liquidity, and value-at-risk (VaR). The haircut is the amount of overcollateralization a counterparty requires for a given piece of collateral. For example, to attain $100 in funding, one might only have to pledge $101 of UST bills, since they are credit risk-free and highly liquid. On the other hand, if one has only BBB rated corporate bonds, one might have to pledge $110 or $120 to attain $100 in funding. Thus, the haircut provides a margin of safety and is used to rank the riskiness of various assets.

Since these are largely short-term funding transactions that are continuously rolled over (usually taking less than 3 months), the things that repo markets care most about are the liquidity and volatility characteristics of the underlying security, not necessarily the credit risk.12 For example, a bank extending funding to a client accepting USTs as collateral does not care that the US government might be bankrupt in 5 years – it is only concerned with the fact that the underlying security will not move very much in the next week or month and that there will always be a liquid market to sell it into if there is a default of debt. Thus, value-at-risk (VaR) defines haircuts based on the historical and statistical volatility of assets.

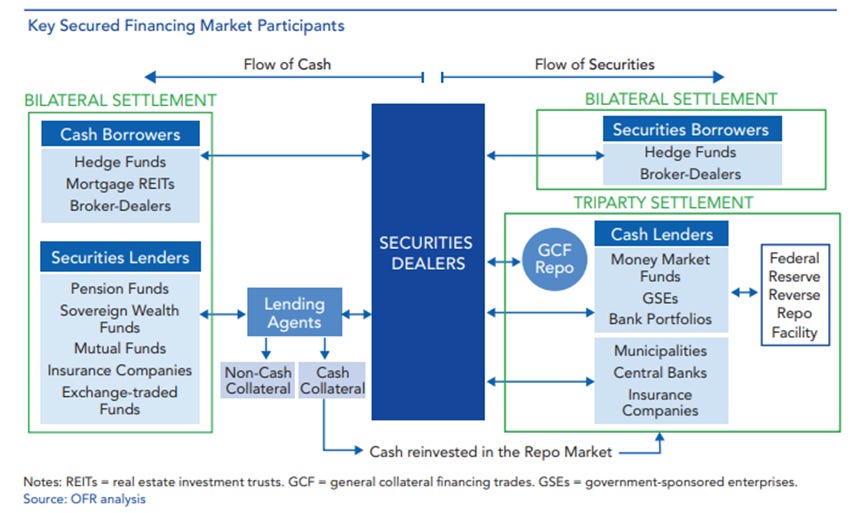

Dealer banks play an integral role in this market, connecting the money and collateral pools. Typically, entities that actually have collateral (insurance funds, pension funds, asset managers, etc.) are not entities that typically rely most on its use (hedge funds, money market funds, dealers, etc.). These collateral holders can “lend” out their collateral to earn extra yield to dealers who then redistribute this collateral to the rest of the system.

Since the supply of high-quality collateral has been insufficient to meet the financial system’s needs for growth and legislative/regulatory purposes, certain financial innovations have facilitated new methods of manufacturing the necessary collateral through something called “collateral transformation.”

Imagine an insurance company that wants to engage in a derivatives transaction. To do so, it is required to post collateral with a clearinghouse, and, because the clearinghouse has high standards, the collateral must be “pristine” – that is, it has to be in the form of Treasury securities. However, the insurance company doesn’t have any unencumbered Treasury securities available – all it has in unencumbered form are some junk bonds. Here is where the collateral swap comes in. The insurance company might approach a broker-dealer and engage in what is effectively a two-way repo transaction, whereby it gives the dealer its junk bonds as collateral, borrows the Treasury securities, and agrees to unwind the transaction at some point in the future. Now the insurance company can go ahead and pledge the borrowed Treasury securities as collateral for its derivatives trade. Of course, the dealer may not have the spare Treasury securities on hand, and so, to obtain them, it may have to engage in the mirror-image transaction with a third party that does – say, a pension fund. Thus, the dealer would, in a second leg, use the junk bonds as collateral to borrow Treasury securities from the pension fund. And why would the pension fund see this transaction as beneficial? Tying back to the theme of reaching for yield, perhaps it is looking to goose its reported returns with the securities-lending income without changing the holdings it reports on its balance sheet.13

The diagram below demonstrates this – simply swap the Argentine government for a risky corporate lender, Bank A for some domestic non-bank, and the orange arrow Eurobond for a diverse assortment of risky assets.

In summary, the financial economy has developed methods of generating and sustaining increased purchasing power that is somewhat loosely tethered to the real economy. In the financial economy, collateral, in the form of liquid assets, serves as high-powered base money that supports leveraged structures and OTC derivatives. While this collateral need not necessarily be high-quality, there must be a liquid market.

Haircuts determine the overcollateralization required for a given piece of collateral. Haircuts are partially determined using value-at-risk (VaR) models, so historical and statistical volatility is imperative.

Rehypothecation allows a single security to serve as collateral in more than one transaction. US short-term funding markets (including tri-party repo) have constraints that check this within the United States, but there are no legislative and regulatory limits on collateral reuse offshore.

Collateral reuse creates collateral chains, which are basically strings of transactions that are supported by a single security. The length of these collateral chains can be called the “velocity of collateral.” Collateral velocity is a confidence measure, meaning that there is no central bank backstop for this collateral-based financial economy.

If there is insufficient high-quality collateral, available market participants can “transform” or “upgrade” low-quality collateral into high-quality collateral through a transaction that fundamentally amounts to a repo transaction that uses non-cash collateral.

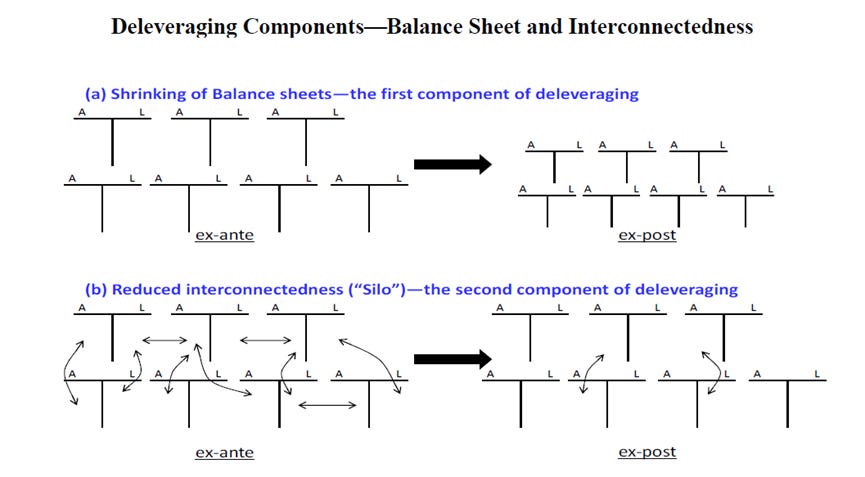

Dealers are required to “source” collateral from “collateral silos” that exist in pension funds, insurance funds, exchange-traded funds, and other financial entities and “mobilize” this collateral so that it can be used for funding at other broker-dealers and hedge funds.

In the event that haircuts increase, the length of collateral chain decreases, the supply of collateral decreases, or dealers are unable/unwilling to mediate and/or transform collateral, and the financial system deleverages. This kind of deleveraging is not as obvious as decreasing a standard leverage ratio. Consequently, decreased collateral velocity, shrinking collateral chains, or an inability/unwillingness to engage in collateral transformation deleverages the financial economy through a reduction of interconnectedness, rather than a shrinking of balance sheets.

Manmohan Singh, Collateral and Financial Plumbing, 2016.

Technically, there are various legal distinctions between rehypothecation and other types of collateral reuse relating to rights to title, ownership, use, etc. However, for our purposes, they are functionally equivalent and I will use the terms interchangeably in this research note.

https://www.federalreserve.gov/econres/notes/feds-notes/ins-and-outs-of-collateral-re-use-20181221.htm

https://voxeu.org/article/other-deleveraging-what-economists-need-know-about-modern-money-creation-process

Ibid.

Manmohan Singh, Collateral and Financial Plumbing, 2016.

I cannot stress enough how tentative these estimates are. Manmohan Singh relies on footnotes in banks annual reports to determine the level of available collateral, but these are only a “snapshot” at year-end or quarter-end, which means banks have already “window dressed” their balance sheets.

https://libertystreeteconomics.newyorkfed.org/2012/06/mapping-and-sizing-the-us-repo-market/

https://ideas.repec.org/p/fip/fednls/86956.html

https://www.financialresearch.gov/working-papers/files/OFRwp-2016-06_Map-of-Collateral-Uses.pdf

https://www.bis.org/publ/qtrpdf/r_qt1709e.htm

This is essentially what happened in the financial crisis of 2007-2008. Illiquid ABS were using leverage provided by the commercial paper market. MMFs that invested in this CP had to value their holdings daily because they need to keep a stable NAV. These ABS were illiquid and did not regularly trade, so they were priced using implied correlation in the Credit Default Swap market. Once the CDS market became illiquid (banks turned from net sellers to net buyers of CDS), the pricing for these illiquid ABS structures went haywire and they were unable to secure funding in the commercial paper market, forcing margin calls. However, very few of these products actually defaulted and caused cash losses for investors. Banks and other participants were simply forced to dump these at any price because the mark-to-market value had fallen so much that it trigged margin calls. This is remarkably similar to the case of Long-Term Capital Management in 1998 – their trades eventually wound up being profitable for the banks who bailed them out, but they were forced out of their positions in the interim due to funding concerns.

https://www.federalreserve.gov/newsevents/speech/stein20130207a.htm

"However, through the repledging and rehypothecation of collateral, and the resultant creation of “collateral chains,” additional purchasing power is created in the financial economy without a need for the creation of any additional bank deposits, bank reserves, government debt, private debt, or anything else for the matter. "

I cannot understand this paragraph. How can I purchase a piece of machinery without writing a check or giving cash to the seller? In my mind, purchasing power is always related to a bank accout or to cash in my pocket...

buen articulo!! saludos desde argentina.